SA

SA  KW

KW  IE

IE AU

AU UAE

UAE UK

UK USA

USA  CA

CA DE

DE  QA

QA ZA

ZA  BH

BH NL

NL  MU

MU FR

FR [ LET’S TALK AI ]

X

Discover AI-

Powered Solutions

Get ready to explore cutting-edge AI technologies that can transform your workflow!

Get ready to explore cutting-edge AI technologies that can transform your workflow!

")

Insurance in the United States has always been built on a promise: protection when it matters most. Yet for many policyholders, the experience doesn’t always live up to that promise.

But if you’ve ever actually filed a claim, you know it doesn’t always feel that way.

Things move slowly. There’s paperwork everywhere. You wait, follow up, wait some more… and half the time, you’re not even sure what’s happening behind the scenes. In moments where you need clarity and speed, the process can feel frustratingly complicated.

That gap between what insurance promises and what people actually experience? It’s getting harder to ignore.

And that’s exactly why the industry is starting to change.

Why does insurance feel the slowest when you need it the most? That’s what Insurtech is trying to fix.

Insurtech companies in USA are finally making it happen. A big part of this change comes down to smart contracts in insurance industry which is backed by innovation from a mobile app development company and emerging tech providers.

Now, instead of relying on back-and-forth approvals and manual checks, imagine policies that just work. Automatically. The moment certain conditions are met, everything triggers on its own.

That’s what smart contracts do.

Built on blockchain technology, they bring something insurance has been missing for a long time: speed, transparency, and a lot less guesswork.

Let’s explore how smart contracts in insurance industry are changing the way insurance actually works.

A smart contract is basically an agreement that runs on its own. No chasing approvals. No waiting around. It just does what it’s supposed to do when the conditions are met.

Now think about how insurance usually works. You file a claim, someone reviews it, then maybe it gets approved. It takes time. Sometimes a lot of it.

With smart contracts in insurance industry, that whole process gets flipped.

Instead of paperwork and back-and-forth emails, everything is already written into code. The terms, the conditions, the payout rules, it’s all predefined. So when something actually happens, the system doesn’t wait. It just acts.

Take a simple example. Say you have travel insurance for flight delays. Normally, you’d have to file a claim and wait for verification.

With a smart contract? It’s different.

The system is already connected to real-time flight data. If your flight gets delayed beyond a certain point, the contract checks it automatically and boom, the compensation is triggered. No forms. No follow-ups.

That’s where blockchain in insurance industry comes in. It makes sure all of this runs on a system that’s secure, transparent, and almost impossible to mess with. Once the contract is live, no one can quietly tweak the rules later.

Suggested Read: Exploring Insurance Policy Management Software: It’s Top Platforms & Our Expertise

How would it feel if insurance in the USA actually worked the way it’s supposed to? That’s the reality of smart contracts.

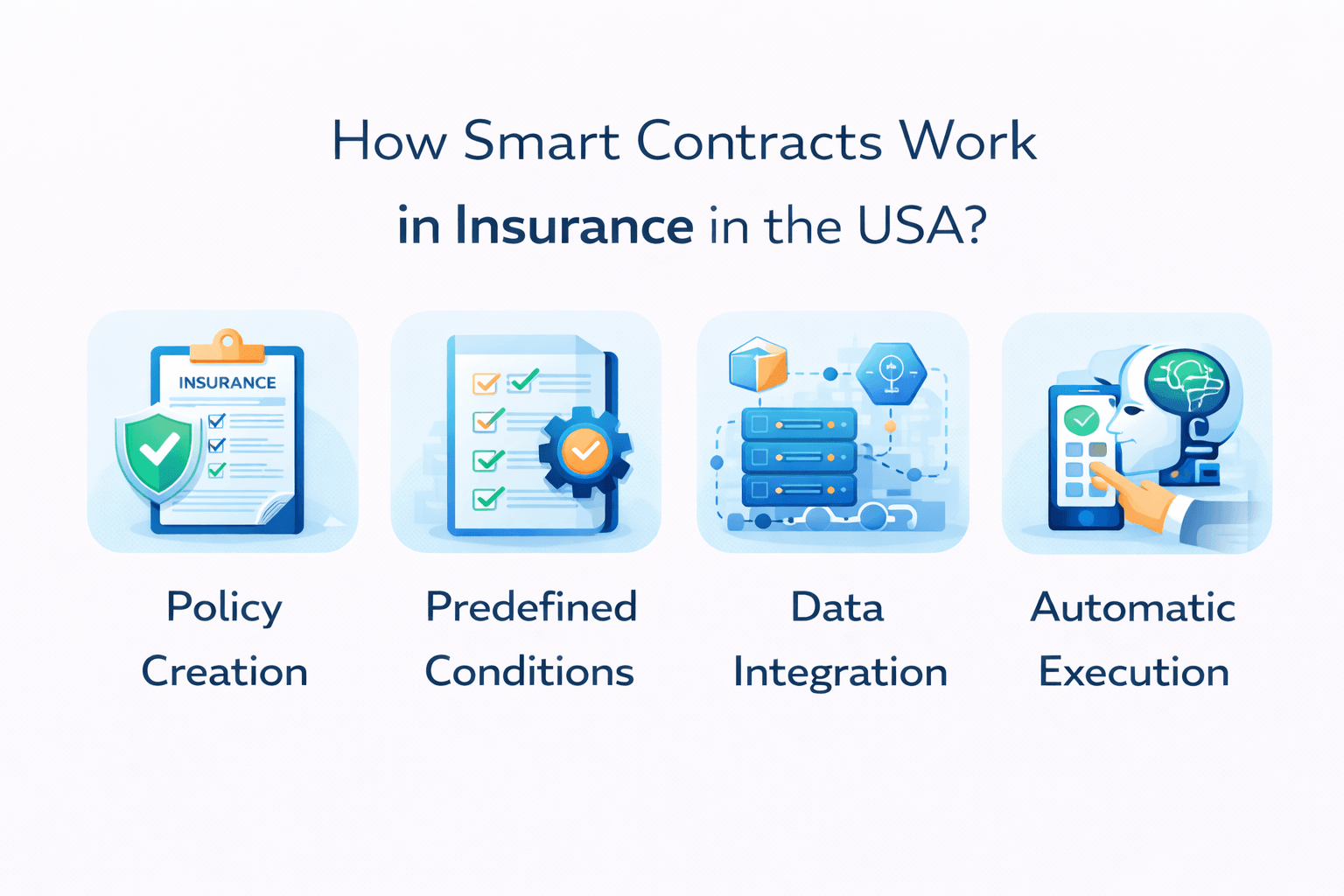

Understanding how smart contracts work in insurance becomes clearer when broken into a structured process.

Think of it like a chain of small steps. One thing happens, then the next. No confusion. No back-and-forth. You’re not dealing with heavy tech here. You’re just setting clear rules in advance, and letting the system handle the rest.

Once you look at it this way, the whole idea feels a lot less technical, and a lot more practical.

First, specific triggers are set. These could be anything from a car accident to a medical treatment, or even a delayed flight. The contract “knows” what counts as a valid event

These triggers are what make the contract actually work. In the USA, they keep things consistent and fair. No guesswork, no arguments. Whether it’s a car accident, a delayed flight, or a medical claim, the rules are simple and clear.

Smart contracts get their information from external sources, often called oracles. These can include live weather data, hospital records, or real-time flight statuses. By feeding verified data directly into the contract, the system can check conditions automatically. No human review needed.

When the defined conditions are met and verified through data inputs, the contract executes automatically. This can include approving a claim or initiating a payment.

This kind of automation makes insurance faster, simpler, and far less frustrating for everyone.

Next, let’s look at real-world examples and use cases where smart contracts are already changing insurance as we know it.

Smart contracts in insurance aren’t sci-fi, they’re real. Also, they’re flipping the insurance world upside down in the USA.

No more waiting weeks for a payout. No more drowning in paperwork. You can now file a claim and have it handled automatically while you’re sipping your morning coffee. That’s what these contracts do.

Want to know how it actually works across different types of insurance? Let’s have a look.

Accident claims in traditional systems can be a nightmare. Inspections, paperwork, approvals that drag on for days or weeks. Smart contracts change that. Data from connected devices or reports can verify an incident instantly, triggering faster payouts. Suddenly, getting your car fixed doesn’t have to feel like pulling teeth.

Healthcare claims are notoriously complex. Multiple stakeholders, layers of verification, endless forms… it’s easy to get lost. Smart contracts simplify this. They validate treatments against predefined rules and can automate reimbursements, cutting down delays and reducing the frustration for patients and providers alike.

This is one of the clearest wins for smart contracts. Imagine a flight delay or cancellation. Normally, you’d have to file a claim and wait. With smart contracts, the system monitors flight data in real time. If a delay happens, compensation is automatically issued.

Life insurance claims can be emotionally taxing, especially when payouts are delayed. Smart contracts can use verified records to initiate payments immediately, ensuring beneficiaries receive support faster, and reducing the administrative bottlenecks that often hold things up.

These examples show how smart contracts in the US insurance industry are turning processes from slow and reactive into fast, automated, and proactive. Insurance isn’t just catching up, it’s finally starting to work the way it should.

Smart contracts in insurance aren’t just theory. Some companies are already putting them to work in the USA.

Take State Farm. They’ve been testing blockchain to make claims and subrogation faster and more efficient.

MetLife is experimenting too, using blockchain to automate parts of policy management and claims.

Then there’s Lemonade. While not fully blockchain-based, they’ve shown how automation can cut claim processing from days to just minutes.

These examples show one thing clearly: the insurance industry in the USA is actively testing and adopting smart contracts. Full-scale use is still growing, but the shift toward faster, automated, and smarter processes is already happening.

And it’s not just companies, experts are seeing the same shift.

“Just a few years ago, the idea of instant, clear insurance seemed far-fetched. Today, smart contracts are changing that in the USA.”

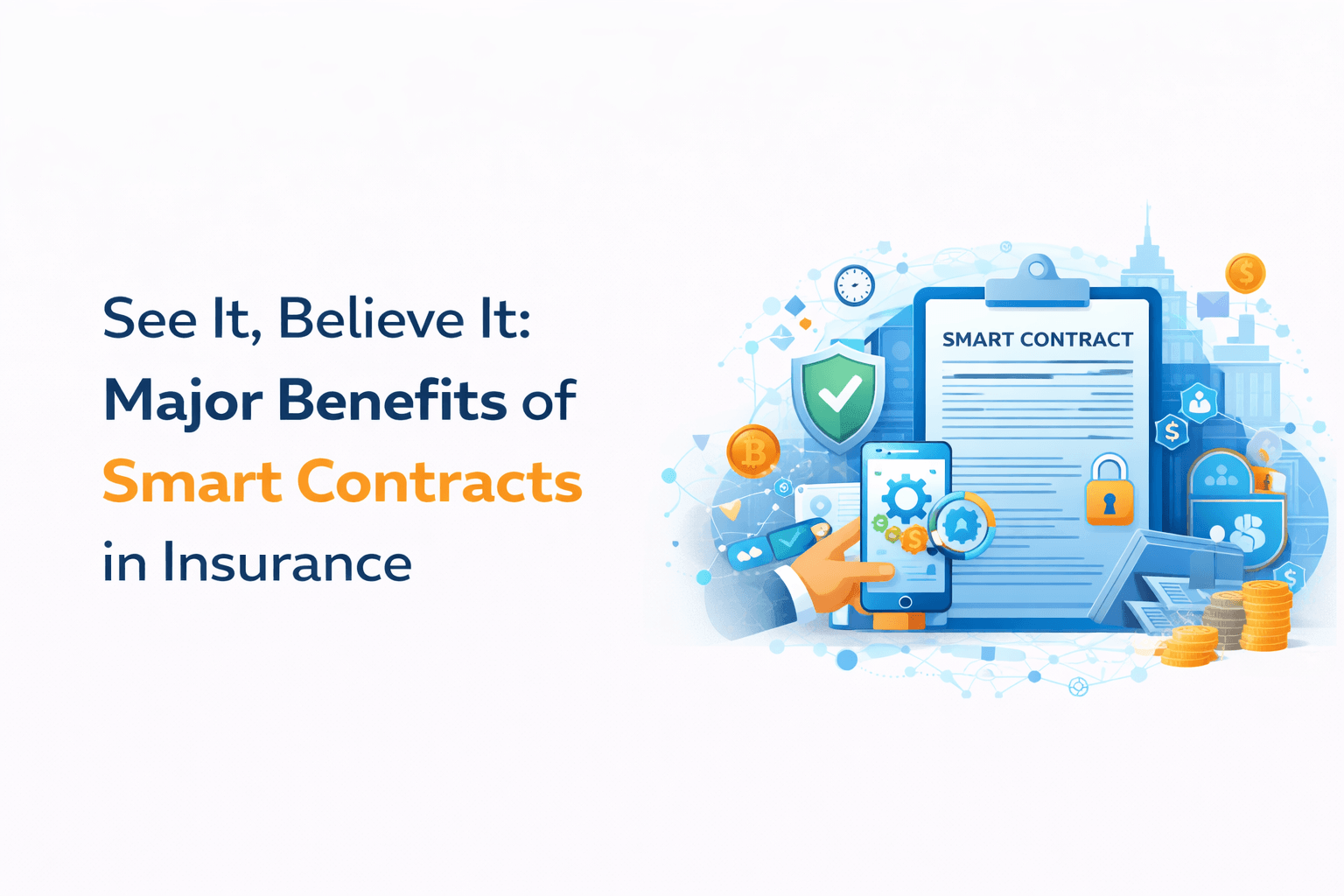

Smart contracts in insurance aren’t just hype. They’re actually making life easier in the USA. Both insurers and policyholders are feeling the difference.

Wondering what the benefits of smart contracts in insurance in the USA are? Here are the top ones you need to know:

Forget waiting weeks for approval. Smart contracts handle everything automatically. Claims get paid faster, and you don’t have to chase anyone.

Everything runs on set rules and verified data. That makes it way harder for fake claims to slip through. Less fraud, more trust.

Less paperwork, fewer manual checks, smaller admin teams. Insurers save money while keeping things smooth and efficient.

Every step is recorded on the blockchain. You can see what’s happening, and so can the insurer. Everyone’s on the same page.

Policyholders get faster, clearer results. No repeated calls, no confusion. Just a simpler, stress-free experience.

These are the reasons why everyone’s talking about smart contracts in US insurance.

In short? Smart contracts in insurance are making the whole system faster, fairer, and more reliable. That’s insurance automation in action, and it’s already changing the game in the US market.

Smart contracts in insurance sound like a game-changer. And honestly? They kind of are. Faster claims, fewer middlemen, and way less paperwork. Who wouldn’t want that?

But let’s slow down for a second.

Like any new tech shaking up a traditional industry, it’s not all smooth sailing. There are some real challenges hiding beneath the surface. Things that need to be solved before smart contracts can truly take over.

Here are some of the key challenges of smart contracts in insurance industry worth paying attention to:

One policy, fifty variations. That’s how insurance works across the USA. Each state has its own rules, and organizations like the National Association of Insurance Commissioners set the standards. Smart contracts have to play by these rules, which can get tricky.

Most insurers still run on old systems. These weren’t built for blockchain. Connecting smart contracts can mean costly upgrades and lots of technical headaches.

Tech is ready, but the law is still catching up. Can a smart contract hold up in court? Who settles disputes if something goes wrong? These questions still need answers.

Smart contracts rely on external data, like weather updates, flight statuses, or hospital records. If the data is wrong, the contract executes wrong. So, remember that accuracy is everything.

These challenges aren’t deal-breakers, they’re hurdles to clear. Address them, and smart contracts can really transform the insurance game in the USA.

When insurance companies in USA want to turn smart contract ideas into reality, they quickly realize it takes more than just blockchain knowledge. You need a partner who can build secure, scalable, and reliable solutions.

That’s where a blockchain app development company in USA like Techugo comes in.

They specialize in creating blockchain-based applications and smart contracts that automate claims, speed up processes, and reduce errors. From concept to deployment, Techugo helps insurers move from theory to real, working solutions.

For any insurer looking to adopt smart contracts at scale, teaming up with a mobile app development company in USA makes sure the technology does what it promises, like speeding up payouts, cutting the red tape, and giving policyholders a seamless, stress-free experience.

With Techugo, slow claims and red tape are officially history, so insurers and policyholders both win.

Smart contracts are computer-based contracts, which operate automatically. In insurance, they are automatic and approve claims or make payouts upon satisfaction of set conditions, which does away with waiting and unnecessary paperwork.

Smart contracts in the United States are based on the blockchain technology to remain secure and transparent. They draw real-time information, e.g., flight delays or medical records, to confirm conditions. After the verification, payments occur immediately, and claims become quicker and less cumbersome.

They speed up claims, reduce errors, lower operational costs, prevent fraud, and improve transparency, and it ends up creating a smoother experience for policyholders in the USA.

Yes! Auto, health, travel, life, almost any type. Some sectors are quicker to adopt it, but the tech fits most insurance cases.

Absolutely. Companies like State Farm, MetLife, and Lemonade are already experimenting with smart contracts to automate claims and policy management, cutting processing times from days to minutes.

Every single day, healthcare companies submit millions of both insurance claims and accounts receivable (A/R) claims. However, when it comes to claims..

Millions of people open mobile apps every day without thinking about what it actually takes to make those apps work. They scroll, swipe, watch videos,..

Write Us

sales@techugo.comOr fill this form