SA

SA  KW

KW  IE

IE AU

AU UAE

UAE UK

UK USA

USA  CA

CA DE

DE  QA

QA ZA

ZA  BH

BH NL

NL  MU

MU FR

FR [ LET’S TALK AI ]

X

Discover AI-

Powered Solutions

Get ready to explore cutting-edge AI technologies that can transform your workflow!

Get ready to explore cutting-edge AI technologies that can transform your workflow!

Do you think that building a fintech app like Citi Mobile requires a huge investment? What if we told you that you simply need $30K to get started? Yes, you have heard that right! Basic mobile applications with essential features can be developed for less than $30,000.

In today’s world, almost everyone is using digital mobile applications. This turns fintech into one of the most lucrative sectors worldwide. You are wrong, though, if you believe that creating a powerful and feature-rich fintech app necessitates an excessive budget. Proper preparation and a dependable mobile app development business will help to create a successful fintech app.

Before delving into sophisticated features, including backend development, API integration, and AI tools, one must grasp the cost structure. This will help you know which features have the most impact on the budget.

Designed by Citibank, the Citi Mobile App lets consumers handle their finances using their mobile devices through a digital banking program. Designed for everyday banking demands, it is a full-service fintech application. Real-time monitoring of credit cards, paying bills, money transfers, and checking account balances are among some of its functionalities. Citi first introduced the Citi Mobile App in the early 2010s as part of its digital revolution plan. Through an encrypted system and APIs, the app gives consumers a secure connection to their financial accounts, therefore guaranteeing safe financial activity. The app has added features including financial insights, instantaneous alerts, and biometric login over time, therefore becoming a practical and secure mobile banking tool for the modern mobile generation.

As the world is moving rapidly into a banking system, fintech apps have become a crucial tool in managing our financial lives. In the U.S., for example, 92% of people use payments and consumers use 3-4 fintech apps for various financial requirements. This presents a business opportunity in this area.

Moreover, younger generations like Millennials and Gen Z are accelerating this trend by using apps like Citi Mobile; 71% of Millennials are open to sharing data to improve their financial services.

Banking Users can check their balances, transfer money and make payments on their mobile phones without having to go to a bank, making it easier and faster to manage finances.

under one roof, Citi Mobile, for example, aggregates banking, credit card, investment and payment services on one platform.

There are also more sophisticated security features, including biometric logins, encryption and real-time alerts, that help build user confidence in mobile banking.

As well as spending insights, trends and analysis, fintech apps also use data and AI to provide smart financial recommendations.

Instant payments, quick transfers, and automated services significantly improve transaction speed compared to traditional banking.

You’ve got the idea now of how powerful fintech apps can be but let’s see how they work, really. If you’re under the impression you have to open a bank or become a financial institution to create an app like this, it’s not necessarily true. The vast majority of fintech applications are built on top of traditional banks and financial institutions rather than being entirely independent, serving as an intermediary between customers and those companies.

Users sign up on the app and complete KYC (Know Your Customer) verification using documents and identity checks.

The app connects with banking systems or financial institutions via APIs to access user account data securely.

All financial data (balances, transactions, cards) is. Displayed on a user-friendly dashboard in real time.

Users can transfer money pay bills or manage cards while the app processes these requests through integrated payment gateways and banking APIs.

Every action is protected with encryption, OTPs or biometrics and users receive alerts for transactions and updates..

Even after the pandemic rebounds, digital finance adoption is still increasing, which means investing in a fintech app today can be a highly scalable opportunity. But it’s wise to plan your budget well before you start working on your product to prevent overselling or underselling.

Choose between launching a full-scale app like Citi Mobile App or a basic version (MVP) with few capabilities. Beginning with an MVP allows you to evaluate the market and lowers first cost.

List must-have features (like login, transfers, dashboard) together with sophisticated features (AI, analytics). This lets you assign money only where it really counts.

Whether you recruit freelancers, have an in-house crew, or subcontract to an agency determines your cost. Your total budget is also greatly affected by your selection of the appropriate technology stack and location (India vs US).

Estimated Cost: $5,000 – $15,000

Features – The aim of this stage is to establish the competitor landscape, target users, business model and development plan. It makes sure your app fits market needs and has a well-defined strategic direction.

Estimated Cost: $8,000 – $25,000

Features – Wireframes, prototypes, and visual designs are included. A user-centered methodology is adopted to help increase engagement, usability, and user experience as a whole.

Estimated Cost: $20,000 – $60,000

Features – Focus on building screens, navigation, and interactive elements for the user. Performs well on multiple devices and platforms.

Estimated Cost: $25,000 – $80,000

Features – Manages server-side logic, databases, APIs and business rules. All the functionalities of the bootsapp runs on this engine.

Estimated Cost: $10,000 – $40,000

Features – This includes the integration of payment gateways, banking APIs and KYC, AML verification, notification, and other necessary services from 3rd parties as required.

Estimated Cost: $15,000 – $60,000

Features – Covers compliance for KYC, AML, GDPR, PCI-DSS and necessary approvals. A legal consultant assists in trouble-free app operations and functioning.

Estimated Cost: $7,000 – $30,000.

Features – It includes manual, automated, and security testing. Ensured the app was free of bugs, reliable, and performed flawlessly on all devices.

Estimated Cost: $5,000 – $20,000

Features – Set up of the server and hosting in Cloud (AWS, Azure, GCP), app store submission, and DevOps pipeline. Guarantees seamless adaptation and growth.

Estimated Cost: $15,000 – $50,000 per year

Features – Involves improvements, fixes, enhancements and addition of features. Maintains the app’s security and stability over time.

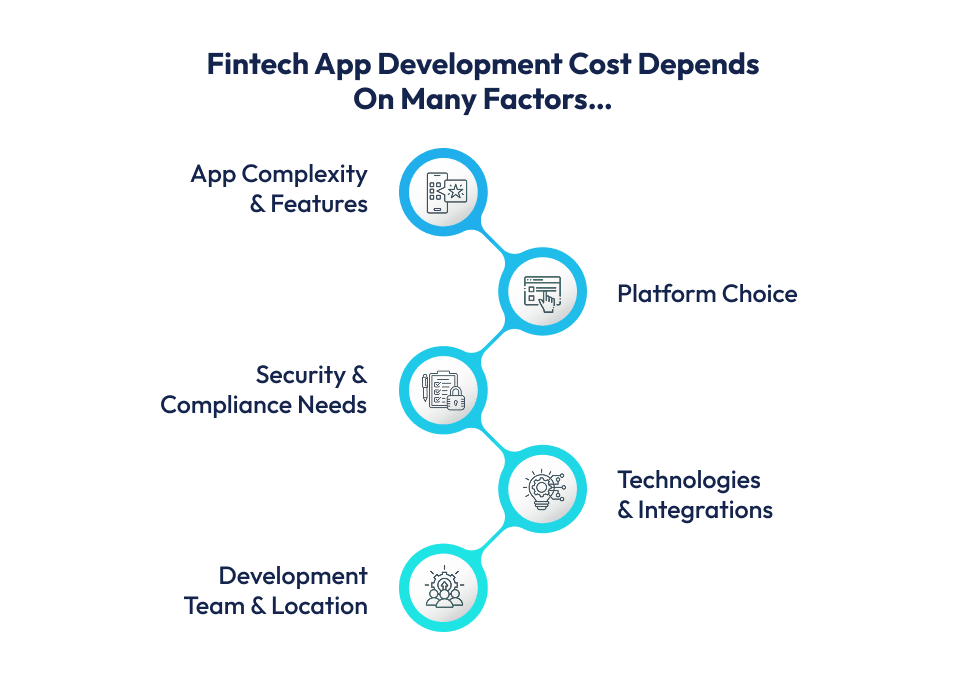

Several factors influence the overall cost of building a fintech app like Citi Mobile App. Understanding these helps you plan your budget more effectively.

| Development Phase | Estimated Timeframe | Description |

| Market Research & Planning | 2 – 4 weeks | Competitor analysis, user research, defining features and business model. |

| UI/UX Design | 3 – 6 weeks | Wireframes, prototyping, visual design, and user experience testing. |

| Backend Development | 8 – 12 weeks | Server setup, database design, API development, and core business logic. |

| Frontend Development (iOS & Android) | 6 – 10 weeks | Coding the user interface, app screens, navigation, and interactive features. |

| API & Third-Party Integrations | 4 – 6 weeks | Payment gateways, banking APIs, KYC/AML verification, and notifications. |

| Security Implementation | 3 – 5 weeks | Encryption, biometric login, fraud detection, and secure transaction setup. |

| Testing & Quality Assurance | 4 – 6 weeks | Manual testing, automated testing, security testing, and bug fixing. |

| Deployment & App Store Submission | 1 – 2 weeks | Publishing on iOS App Store and Google Play Store with final checks. |

| Maintenance & Post-Launch Updates | Ongoing | Regular updates, bug fixes, performance optimization, and feature enhancements. |

Managing overall cost is also a crucial step when building a fintech app like Citi Mobile App. Smart planning and strategic decisions can help you save significantly without compromising quality.

Choose a development partner who has already built fintech applications. Such a partner removes the need for experiments, keeps the schedule intact and uses budget plus staff with maximum efficiency. The same partner already knows the compliance rules and the security requirements – the project avoids extra audits but also rework.

Start with a fundamental version including only the fundamental features. Launch this edition first to gauge market interest and gather user feedback. Include the more advanced capabilities in later revisions. This method keeps you from spending big upfront on choices that eventually turn useless

Rather than creating everything by yourself, utilize secure third-party APIs for payments, KYC identity verification, notifications and analytics. This ensures reliable performance at a lower development cost and faster time to market.

Concentrate on the core features that address the primary user pain point and push nonessential features to subsequent releases. Prioritization guarantees that your budget is used for features that actually provide value.

By hiring developers from cheaper countries or using a hybrid (on-site + outsourced) team, you may substantially reduce labor costs without sacrificing quality.

Develop the app’s framework for future expansion instead of overloading it at first. An extensible architecture helps to bypass expensive redesigns or server upgrades down the line.

This plan keeps the project within budget while still balancing usability, security, and quality.

One of the most important developments molding the fintech sector’s future is the inclusion of artificial intelligence (AI), especially generative AI, as it is changing quickly. These developments are changing user interactions with banking services, investment decisions, and money management style.

AI algorithms can forecast upcoming expenditures, study spending patterns, and offer individualized budgeting guidance. Generative AI carries this even more by automatically producing personalized financial reports, notifications, and investment recommendations.

Automatically suggesting asset allocations, risk analysis, and investment approaches are artificial intelligence-driven fintech applications. For consumers, generative artificial intelligence can generate predictive market insights and simulation models.

Smart chatbots powered by generative artificial intelligence can process transactions, manage difficult questions, and even provide proactive recommendations.

Real-time prediction of credit risks, detection of suspicious transaction patterns, and detection of possible fraud are among AI’s uses. To improve security measures, generative artificial intelligence models can simulate possible fraud situations.

Generative AI can power voice assistants that understand natural language and execute banking operations seamlessly. Users can ask questions, make transfers, or check balances using simple voice commands.

Overall Trend: Integrating AI and Generative AI into fintech apps may increase initial costs by 20–40%, but it significantly enhances user engagement, personalization, security, and operational efficiency. In the next 3–5 years, AI-powered fintech apps are expected to dominate the market, with higher retention rates, smarter financial services, and stronger competitive advantage.

Almost 9 in 10 Americans now use some form of fintech service, showing the growing demand for digital banking apps. Building a fintech app like Citi Mobile App can cost anywhere from $50,000 for an MVP to $500,000+ for a full-scale app, depending on features and complexity.

Partnering with a reliable team like Techugo ensures your app is secure, compliant, and user-friendly while optimizing costs and time-to-market.

Ready to build your fintech app? Contact us Techugo today and turn your idea into a powerful digital banking solution!

Apps like Kling AI can generate videos in seconds. But do you know the actual cost to build an app like Kling AI that runs technology this advanced? ..

The doctor questions, “When was your last test?” and before you can respond, reports from other hospitals you've visited are displayed on the screen. ..

Write Us

sales@techugo.comOr fill this form