SA

SA

KW

KW

IE

IE AU

AU UAE

UAE UK

UK USA

USA

CA

CA DE

DE

QA

QA ZA

ZA

BH

BH NL

NL

MU

MU FR

FR

Not long ago, banking meant waiting (long queues, slow approvals, endless back-and-forth). Now? It’s instant.

Just think about how things used to work.

Waiting days for approvals, calling customer care for the smallest things, and double-checking every transaction manually. Now you open an app, tap a few times, and it is done.

So what changed?

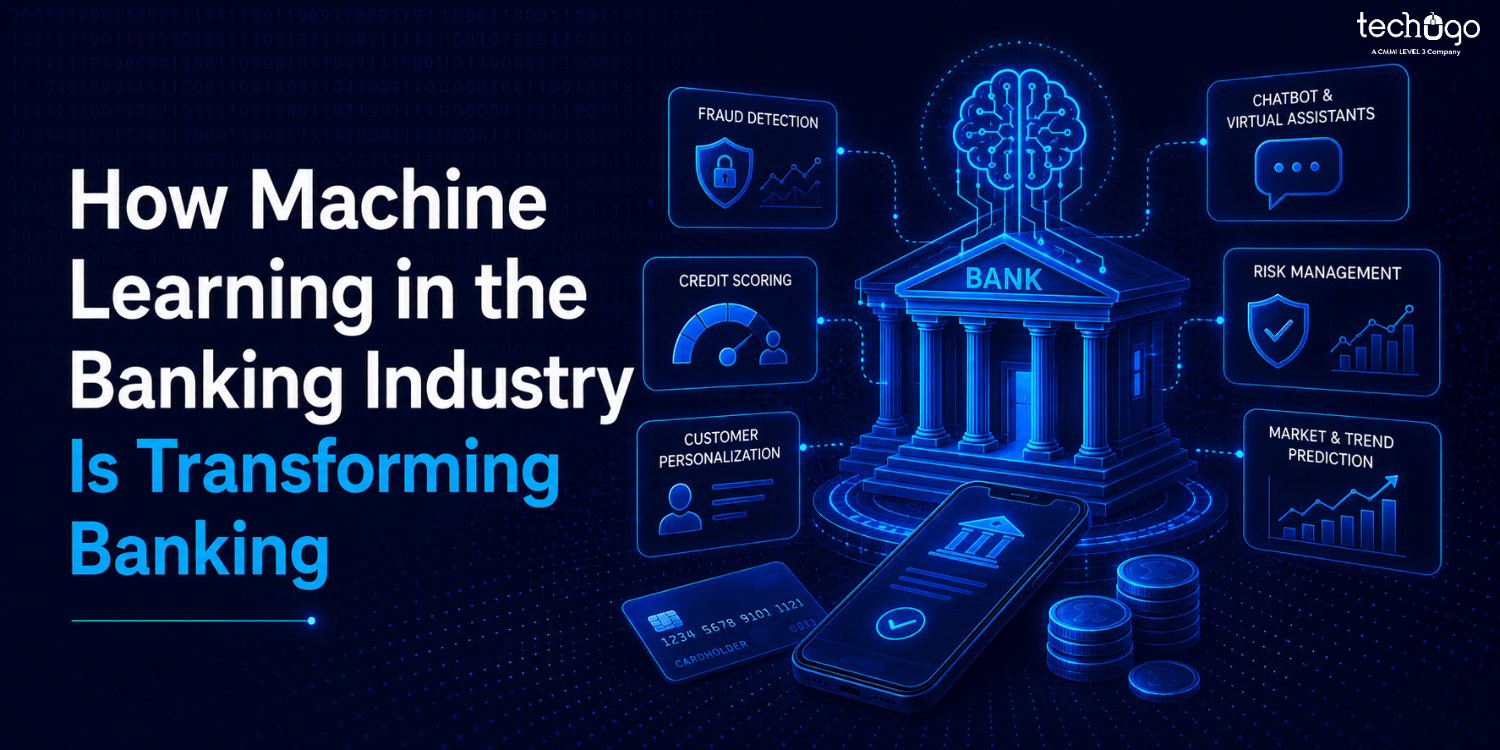

A big part of it is AI. More specifically, machine learning in the banking industry.

And you’ve already seen it in action, whether you noticed or not. That instant fraud alert that saved you from a sketchy transaction? That loan approval that came through way quicker than expected? Those “we think you might like this” suggestions that actually make sense?

Yes, it is machine learning quietly doing its thing in the background.

The interesting thing is that banks are not just collecting data anymore. They are basically learning from it. Every transaction, every click, every behavior pattern… it all adds up. Machine learning looks at all that data and helps banks make better decisions, move faster, and create experiences that feel more ‘you.’

In this blog, we are going to break it all down. What machine learning actually means in banking, why it matters, the real benefits it brings, and how it’s being used across the industry. We’ll also touch on the challenges and what businesses can do to stay ahead.

So, let’s start…

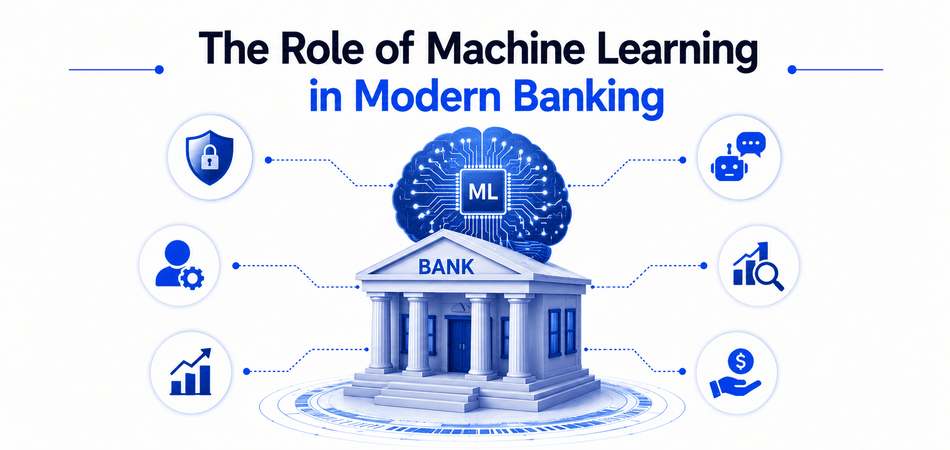

What is Machine Learning in the Banking Industry?

At its core, machine learning in the banking industry is about teaching systems to learn from data instead of relying on fixed instructions. Instead of telling a system exactly what to do in every situation, banks feed it data, and then it figures out patterns on its own.

Sounds complex, but it’s actually pretty simple.

Do you think someone is sitting there checking every transaction one by one? No. Let’s say a bank wants to detect fraud. Instead of manually checking every transaction, a machine learning model studies past transactions. They do not depend on hardcoded rules like “if this happens, do that.” Banks feed the system data. Lots of it. And over time, it starts noticing patterns. What’s normal, what’s not, what looks risky, what doesn’t. Basically, it learns.

That’s pretty much the whole idea.

Data goes in → patterns get picked up → smarter decisions come out.

So why are banks leaning into this so heavily? Because it just makes things easier. Less manual work. Fewer errors. Way faster processing. And the ability to handle millions of data points without slowing down.

And honestly, without it, keeping up with today’s digital banking demands would be nearly impossible.

Benefits of Machine Learning in Banking: What’s Actually Changing

What do banks actually gain from all of this? A lot more than just speed. The real value of machine learning in the banking industry shows up in how decisions are made, how risks are handled, and how customers experience everyday banking.

Here’s a closer look at the benefits of machine learning in banking:

Improved Decision-Making

Banks deal with huge amounts of data every single day. And it is far too much to be realistically processed by any team. Machine learning slices through that noise and assists in transforming raw data into clear and useful information. That way, rather than making decisions based on guesswork, banks will be able to base their decisions on real patterns and trends. The decisions are quicker, smarter, and much more reliable, whether it is granting loans, evaluating risk, or uncovering opportunities.

Greater Security and Fraud Prevention

Security is something that banks cannot afford to get wrong. Machine learning maintains a regular vigilance on transactions, and it identifies anything abnormal as soon as it occurs. And yet it does not end there. It studies every new case and becomes more proficient at detecting threats. It implies that fraud is discovered at an earlier stage, the number of false alarms is minimized, and the customers will feel safer knowing that their money is secured without frequent disruptions.

Moreover, sophisticated algorithms can be used to examine patterns of millions of accounts, which can point to anomalies that otherwise would remain unnoticed by human employees. They are in a position to identify the small traces of identity theft, suspicious spending patterns, or hacked accounts, and this is usually before they make a loss.

Cost Minimization and Operational Efficiency

Manual processes take time, effort, and a lot of resources. The repetitive tasks can be automated with the help of machine learning, and the teams can be dedicated to more significant tasks. The result? Reduced operational expenses, reduced mistakes, and improved workflows. Systems operate faster in the background, rather than slowing things down, and all things continue moving without additional effort.

And not only that, predictive analytics enables banks to know when operations will be bottlenecked and plan to staff and resource accordingly. This not only increases efficiency with time but also increases the capacity of the bank to scale operations without a corresponding increase in costs.

Personalization of Services

We are not supposed to like generic recommendations, right? Machine learning allows banks to know what customers need, as they are expected to do. This behavior and preference analysis will help banks provide recommendations that are genuinely sensible (a savings plan, a loan proposal, or even a spending plan). It is not so much about marketing products but more about experiences that are relevant and really useful.

Banks can also give timely advice on life events, on top of this, using machine learning. To illustrate, when a customer begins to save to buy a home, the system can suggest mortgage products/investments that suit his or her financial profile.

Faster Processing and Automation

Speed matters, especially in banking. Machine learning helps speed up everything from onboarding new users to processing transactions and approvals. What used to take hours (or even days) can now happen in minutes, sometimes instantly. And the best part? It all happens smoothly in the background, making the entire experience feel effortless for the user.

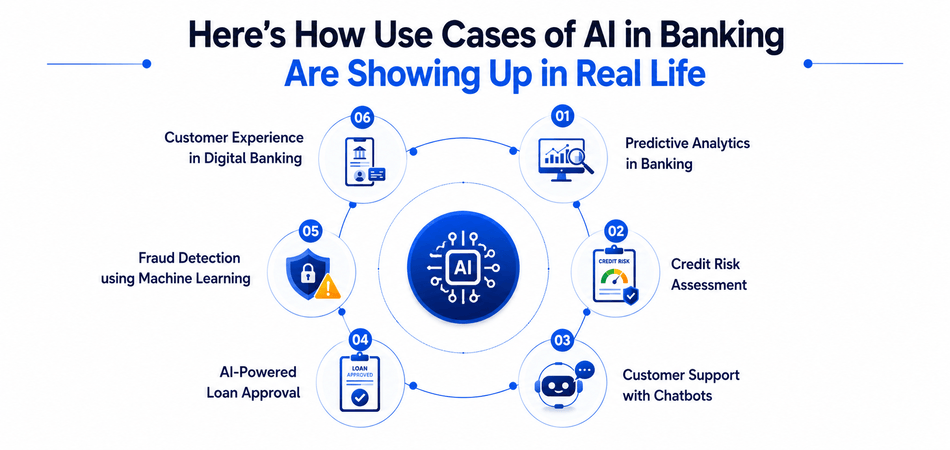

Here’s How Use Cases of AI in Banking Are Showing Up in Real Life

So, what do AI use cases in banking actually look like? From spotting fraud before it happens to predicting what you might need next, AI is quietly making banking faster, smarter, and more personal.

Let’s take a closer look at how it’s really being used.

Predictive Analytics in Banking

Banks don’t guess anymore; they make predictions.

With Predictive Analytics in Banking, banks are able to not only react but actually see what is to be expected. They are able to predict trends, consumer behavior and evaluate credit risk more effectively. As an example, a bank may identify the customers who may require a loan in the near future or those who may cease using the services.

Such foresight assists in keeping the banks one step ahead rather than always responding.

Fraud Detection using Machine Learning

Technology is getting smarter. But so are fraudsters. Fraud Detection Using Machine Learning spots patterns that humans might easily miss. Each and every action is tracked in real-time, and thus, a suspicious activity (such as a purchase of a high value that was not planned, activity in a new area, unusual account behaviour, etc) is marked in real-time.

And even better, it minimizes false alarms, i.e. less unnecessary blocked transactions and a more enjoyable customer experience. Banks are able to respond more quickly, avoid losses, and retain trust without slackening user experience. Concisely, it ensures that banking is safer, and it is still smooth for all users.

Customer Experience in Digital Banking

This is the point where the users actually see the difference. Personalization is changing Customer Experience in Digital Banking. Applications have the ability to recommend products that are, in fact, a good fit with the user, send intelligent suggestions on how to spend, and offer a cohesive cross-device experience. It is not only about functionality anymore, but about rendering banking to be a seamless, intuitively natural experience and even a little smarter than you thought.

Extra Ways AI Is Making Banking Smarter

Beyond the major ones, machine learning in the banking industry is improving multiple areas:

- Chatbots that handle queries instantly, 24/7

- Loan approvals that happen faster with better accuracy

- Risk management systems that predict and prevent issues before they happen

Put it all together, and one thing’s clear… that AI is not optional anymore. It’s quickly becoming the backbone of modern banking.

Unexpected Challenges of Using Smart Machines in Banks

Like any powerful technology, machine learning comes with its own set of challenges:

Data Privacy Concerns

Banks handle incredibly sensitive financial data, which makes privacy non-negotiable. Machine learning systems need access to large amounts of information to work effectively, but that also raises questions: Who can see this data? How is it stored? How long is it kept? Ensuring strict security, transparency, and compliance with regulations like GDPR isn’t just a checkbox; it’s critical for maintaining customer trust.

Integration with Legacy Systems

Not every bank has a modern tech stack. Older systems weren’t designed with AI in mind, which can make integration tricky. Connecting machine learning tools to legacy software can require custom solutions, extra testing, and careful planning to avoid disruptions. It’s a challenge, but one that banks need to tackle if they want to stay competitive.

High Implementation Costs

Setting up machine learning in the banking industry isn’t cheap. There’s hardware, software, cloud services, and the cost of hiring skilled professionals to build and maintain these systems. While the long-term benefits often outweigh the initial expense, the upfront investment can be daunting, especially for smaller institutions.

Need for Skilled Talent

Machine learning isn’t plug-and-play. Banks need data scientists, ML engineers, and AI specialists to create, fine-tune, and monitor these systems. And right now, experts with this kind of experience are in high demand, which means recruiting and retaining top talent is a major challenge for many organizations.

Sure, these challenges can feel overwhelming. Getting AI and machine learning to actually work in a banking app is not always easy. That’s why working with a fintech app development company can make this process a lot more manageable.

Techugo: Making Machine Learning Work in Real Banking Apps

Want your banking app to actually use AI and machine learning without headaches? Techugo can help.

As a trusted mobile app development company, Techugo helps businesses design and build apps that are fast, secure, and user-friendly. Our services cover the full spectrum of app development from UI/UX design and cross-platform development to backend architecture and cloud integration. Every app we create is built for how users interact today, ensuring seamless experiences that feel intuitive and effortless.

Our team also specializes in advanced fintech solutions, integrating machine learning capabilities like fraud detection, predictive analytics, and personalized recommendations. Our focus is on creating apps that don’t just function but adapt, scale, and grow with your business, turning complex technology into simple, impactful experiences for real users.

So are you looking to build something that doesn’t just function but actually stands out? Team up with Techugo, because the right innovation starts with the right team.

FAQs

Q1: What is machine learning in the banking industry?

The concept of machine learning in the banking industry is concerned with teaching machines to learn from data rather than through fixed rules. Algorithms receive data input by the banks, which is then identified by the algorithms to discern patterns, anticipate customer actions, evaluate risk, and detect fraud (all automatically). This assists financial institutions in making wiser decisions in a shorter period and offers more personalized services.

Q2: What are the key benefits of machine learning in banking?

The advantages are revolutionary. Machine learning also enhances decision-making, increases the process speed, such as loan approvals, improves fraud detection, lowers operational expenses, and forms personalized customer experiences. Concisely, it transforms raw data into actionable insights, which provides banks with a competitive advantage in the modern, dynamic digital environment.

Q3: How are banks using predictive analytics?

Banking predictive analytics allows banks to predict trends, customer needs, and credit risks. As an illustration, banks are able to know which customers are in need of a loan in the near future or identify early churn. This proactive strategy assists banks in remaining ahead, making better decisions, and offering to individual customers.

Q4: How does fraud detection using machine learning work?

Machine learning algorithms analyze the data of past transactions in order to identify tendencies that could potentially point to fraud. They detect real-time activity, identify suspicious transactions, and minimize false positives. Unusual card activity and attempts to steal identity are just some of the ways these systems assist banks to avoid losses but maintain the customer experience as smooth and uninterrupted.

Q5: How does machine learning improve customer experience in digital banking?

By providing customer experience in online banking, apps have the capability to make personalized recommendations, intelligent notifications, and cross-platform interactions. Machine learning enables banks to know how customers act and what they like, and it is a frictionless and intuitive experience. The customers feel empathetic, active, and empowered.

Get in touch

We'd love to hear from you.