SA

SA

KW

KW

IE

IE AU

AU UAE

UAE UK

UK USA

USA

CA

CA DE

DE

QA

QA ZA

ZA

BH

BH NL

NL

MU

MU FR

FR

📌 Key Takeaways

- Fintech development outsourcing is now a strategic move, not just a cost-cutting option.

- Demand for fintech software outsourcing is rising due to speed, scalability, and access to niche talent.

- Security, compliance, and system design are the most important parts of any fintech product.

- Fintech projects take longer than expected when teams don’t define scope and compliance upfront

Not that long ago, if you wanted to build a fintech product, you basically had no choice but to hire a full in-house team, pour money into infrastructure, and settle in for a long wait (sometimes a year or more) before you even had something to show. That’s just how it worked.

But frankly? That world feels pretty distant now.

The pressure to ship fast is relentless. Nobody has the luxury of waiting six months to find the right backend engineer or compliance specialist. Whether you’re building a digital bank, a payments tool, a lending app or an investment platform, companies are increasingly relying on fintech development outsourcing to move faster and stay flexible.

And here’s what’s shifted: this isn’t really about cutting costs anymore. Sure, that used to be the whole pitch. But what’s actually driving it now is access — access to specialized talent you can’t easily find locally, the ability to scale your team up or down as things change, and a much faster path to getting something live that’s actually secure and compliant.

So the debate around whether outsourcing “works” in fintech? That’s kind of settled at this point.

The more interesting question (the one actually worth asking in 2026) is how you do it well. Because done right, it’s a serious competitive advantage. Done poorly, it’s an expensive headache.

So in this guide we will explore the state of fintech software outsourcing in 2026, its benefits, popular use cases, challenges, costs, and the key factors to consider when choosing the right outsourcing partner.

The state of fintech outsourcing in 2026

The fintech space has changed. Speed used to be a differentiator – now it’s just the baseline. Customers expect more, products are launching faster – and the competition isn’t just coming from traditional players anymore. And because of that, doing everything in-house starts to look less like a strength and more like a bottleneck.

That’s a big part of why fintech development outsourcing has picked up so much steam.

Companies aren’t turning to outside partners because they lack capability – they are doing it because it’s simply smarter. You get access to specialized talent, you move faster and you can scale when an opportunity shows up instead of scrambling to hire for it.

The numbers back this up too. Fortune Business Insights that the U.S. fintech market is projected to reach $99.82 billion in 2026, while the global fintech market is expected to grow to USD 143.72 billion in the same period.

That’s a lot of ground to cover – and as a result, fintech software outsourcing has become how a lot of companies keep pace without letting hiring cycles or resource gaps hold them back.

What’s interesting, though, is the shift in how people actually think about it. Fintech outsourcing used to feel like a workaround – something you reached for when you couldn’t staff up fast enough.

Now, however, it’s starting to look much more like a deliberate strategic choice – and fintech software outsourcing, specifically, is increasingly where that strategy takes shape, with companies bringing in specialized development partners to build, maintain, and scale the software layer that modern financial products run on. The teams moving quickest right now tend to be the ones who’ve figured out what they should own internally and what’s better off in the hands of a partner who lives and breathes this stuff every day. In other words, knowing where to draw that line has become an advantage in itself.

The real benefits of fintech development outsourcing

The case for outsourcing in fintech isn’t complicated – it comes down to building better products, faster, without the overhead that slows most in-house teams down. Here’s what companies actually gain when they make the shift.

Access to specialized talent

Fintech is a niche space. Finding developers who understand payment infrastructure, regulatory frameworks, and financial security isn’t like hiring general software engineers. Fintech development outsourcing, therefore, opens up a global talent pool of specialists who’ve already built this stuff – no lengthy hiring cycles, no ramp-up time, no hand-holding.

Faster time to market

Speed matters in fintech. Whether you’re launching an MVP development project or rolling out a full product, an outsourced team that already has the processes, tools, and domain knowledge in place moves significantly faster than one being built from scratch. And that gap in delivery time? It can be the difference between capturing a market opportunity and watching a competitor take it.

Cost efficiency

Building an in-house fintech team is expensive: salaries, benefits, infrastructure, training. But fintech outsourcing solutions convert that fixed cost into a flexible one. Companies pay for what they need, when they need it, which makes a real difference especially for startups and scaling businesses watching their burn rate closely.

Scalability on demand

Business needs shift (sometimes overnight). A product launch, a new market, a regulatory change can spike resource requirements faster than any hiring process can keep up with. Outsourced teams, therefore, scale up or down without the friction of layoffs or long recruitment cycles, keeping operations lean without sacrificing capacity when it actually matters.

Access to latest technologies

A good fintech app development company isn’t waiting to be told what tools to use. They are already working with the latest in AI, blockchain, open banking APIs, and compliance automation. But what makes fintech development outsourcing valuable isn’t just the technology itself – it’s that expertise transferring directly into the products they build for you, without the learning curve that comes with developing that knowledge internally.

Reduced technical debt

A lot of fintech companies are still running on infrastructure that was never built for the pace or complexity of today’s market. Legacy system modernisation, therefore, becomes inevitable – but rather than patching systems that were never designed to scale, outsourcing gives companies access to partners who can identify and address those underlying issues properly. The result is cleaner architecture, fewer workarounds, and systems that don’t quietly become a liability six months down the line.

Reduced risk

In-house teams, however talented, are still going to make mistakes that experienced outsourcing partners already have behind them. That institutional knowledge, therefore, translates into fewer missteps around security vulnerabilities, compliance gaps, and architecture decisions that quietly become expensive to undo down the line.

Focus on core business

But perhaps the most underrated benefit is simply this: outsourcing the development layer frees internal teams to focus on what actually drives the business. Product strategy, customer relationships, market expansion. The execution gets handled. The vision, therefore, stays exactly where it should – in-house.

Popular fintech development outsourcing use cases

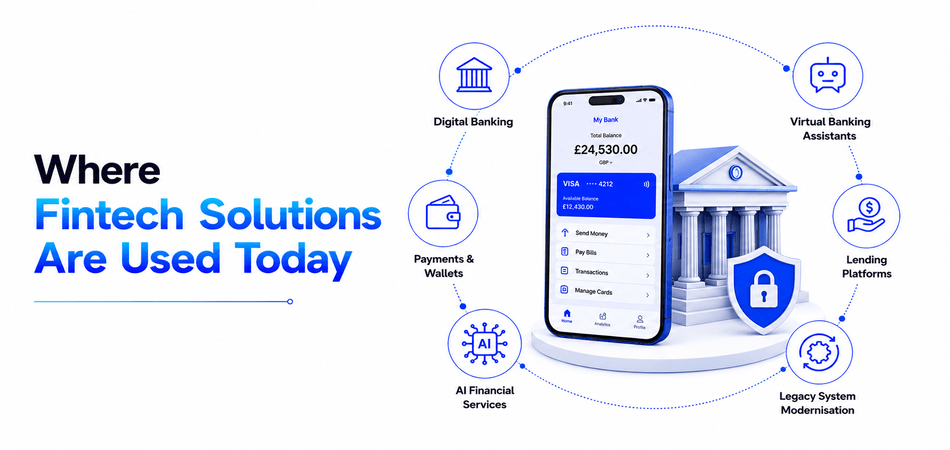

Digital banking platforms

Let’s be honest… most people haven’t walked into a bank branch in years. That’s exactly why so many financial institutions are turning to fintech development outsourcing to build the kind of digital banking experiences customers actually expect. We’re talking mobile apps where you can check your balance at 2 AM, neobanking platforms built entirely without a physical branch, and online portals that put full account control in your hands. It’s not a nice-to-have anymore. It’s the baseline.

Examples: mobile banking apps, neobanking platforms, online account management portals

Payment and digital wallet solutions

Cash is becoming an afterthought. One of the biggest drivers behind fintech outsourcing today is the demand for payment infrastructure that just works instantly, securely, and without friction. Peer-to-peer transfers, tap-to-pay, merchant gateways, digital wallets – building all of this in-house is a massive lift, which is why so many companies are bringing in specialized teams to get it right.

Examples: digital wallets, peer-to-peer payment apps, contactless payment solutions, merchant payment gateways

AI-powered financial services

The way AI in fintech is reshaping risk and decision-making is genuinely hard to overstate. Fraud detection that flags suspicious activity in milliseconds. Credit scoring that goes beyond a three-digit number. Predictive analytics that help institutions stay ahead of what’s coming. None of this replaces human judgment entirely, but it makes that judgment faster and a lot more informed.

Examples: fraud detection systems, AI-based credit scoring, predictive financial analytics, personalized investment recommendations

AI assistants and virtual advisors

More organizations are working with fintech AI product developers to build virtual assistants that do more than answer basic FAQs. When done well, an AI banking assistant can handle account queries, guide users through financial decisions, and escalate to a human when it actually matters. The goal isn’t to remove the human touch — it’s to make sure it shows up where it counts.

Examples: AI chatbots for customer support, virtual banking assistants, automated financial advisors, voice-enabled account management tools

Lending and loan management platforms

The traditional loan process was slow, paper-heavy, and often frustrating for everyone involved. Digital lending platforms have changed that – automated underwriting, streamlined approvals, cleaner repayment workflows. Fintech outsourcing has been a big part of how lenders have managed to modernize here without rebuilding everything from scratch.

Examples: digital loan application platforms, automated underwriting systems, loan approval workflows, repayment management solutions

Upgrading outdated financial infrastructure

This one doesn’t get enough attention. A lot of financial institutions are still running core systems that were built decades ago – and those systems were never designed for APIs, cloud infrastructure, or the pace of modern product development. Legacy system modernisation is rarely glamorous work, but it’s often the most critical. Migrating to the cloud, replacing outdated software, connecting old systems to modern APIs – none of it is simple, but you can’t build the future on a foundation that was never meant to support it.

Examples: migrating core banking systems to the cloud, replacing outdated software, modernizing payment infrastructure, integrating legacy systems with modern APIs

How to successfully outsource a fintech project

Start by getting crystal clear on what you need

Before you reach out to a single vendor, get your requirements in order. What are you actually building? What integrations matter: payment rails, KYC, open banking APIs? What does your timeline realistically look like? Vendors can smell a vague brief from a mile away, and it never ends well for either side. Good fintech product development doesn’t start with a vendor call. It starts with clear goals, honest requirements, and a roadmap you can actually defend.

Pick a model that actually fits your situation

Dedicated teams make sense if you’re building something long-term. Fixed-scope works when your requirements are locked in and unlikely to shift. Staff augmentation is the right call when you just need to fill a specific skill gap fast. Don’t pick a model because it’s trending – pick the one that matches where your product and your business actually are right now. That’s honestly where most fintech development outsourcing decisions go wrong: people copy what worked for someone else instead of thinking it through for themselves.

Evaluate development partners carefully

Anyone can show you a pretty case study. Dig deeper. Have they built payment platforms? Lending tools? Digital wallets? The best fintech outsourcing solutions come from partners who genuinely understand how financial products work – the edge cases, the regulatory constraints, the stakes involved. Generic software experience just doesn’t cut it here.

Validate security and compliance expertise

If a potential partner gets vague when you bring up PCI-DSS, SOC 2, or GDPR, that’s your answer right there. When you outsource fintech development, you’re handing another team access to sensitive financial data and customer information. That’s not something you figure out later – it has to be front and center from day one.

Grow the partnership deliberately

Start small. A pilot, a proof of concept, an MVP app development – something that lets both sides figure out how you work together before the stakes get high. Most businesses that take a thoughtful approach to the outsource of fintech development and scale gradually end up in a much better place than those who rushed into a large engagement too early. Trust takes time. Build it intentionally.

Types of fintech development outsourcing models

There’s no single way to outsource fintech development – it really depends on how much control, flexibility, and budget you’re working with. But generally, most businesses fall into one of these models:

- Project-based – you hand off a defined scope, they deliver. Simple, clean, but less flexible if things change

- Dedicated team – you get a full team working exclusively on your product. More control, better alignment, and honestly the most popular for long-term fintech builds

- Staff augmentation -you plug external talent into your existing team where you need it most

Pick based on your timeline, not just your budget.

Fintech development outsourcing process step-by-step

If you’ve never outsourced a fintech project before, the whole thing can feel like a lot. But honestly, when it’s broken down properly it’s way less intimidating than it looks.

Here’s how the process actually goes:

Step 1. Define what you actually need

This is the step most people rush and then regret. Before you reach out to a single agency, get genuinely clear on what you’re building, what your budget looks like, and what your timeline actually is – not the optimistic one, the realistic one. The more specific you are at this stage, the better every conversation that follows will be. Vague briefs lead to vague proposals, and that never ends well.

Step 2. Research and shortlist partners

Don’t just Google and go with whoever ranks first. Take your time here. Look at portfolios, dig into case studies, and read third-party reviews on platforms like Clutch. And specifically look for fintech experience – this is a heavily regulated, high-stakes space, and a team that’s never navigated compliance requirements or financial data security before is going to learn on your dime.

Step 3. Evaluate and interview

Once you’ve got a shortlist, get on calls. Ask hard questions about their process, their past projects, and how they handle problems when things don’t go to plan – because they never perfectly go to plan. Pay close attention to how they communicate. A partner that asks smart questions back is usually a much better sign than one that just tells you what you want to hear.

Step 4. Sign contracts and NDAs

Before you share anything sensitive (and in fintech, almost everything is sensitive) get the paperwork sorted. Non-disclosure agreements, IP ownership clauses, data protection terms – none of this is optional. A serious development partner won’t flinch at this step, and if they do, that tells you something important.

Step 5. Kick off and align

Once everything’s signed, onboarding matters more than most people give it credit for. Set up shared tools, establish clear communication channels, agree on how often you’ll check in, and make sure everyone is aligned on milestones from day one. A messy kickoff usually leads to a messy project, so take this seriously even if it feels like admin.

Step 6. Build, review, iterate

This is the longest phase and the one where staying involved really pays off. Don’t just hand things over and wait for a finished product. Regular check-ins, sprint reviews, and honest feedback loops keep things on track and catch problems before they become expensive ones. The best outsourcing relationships feel collaborative, not transactional.

Step 7. Launch and hand over

When you’re ready to go live, don’t rush it. Test thoroughly, deploy carefully, and make sure all documentation – technical docs, user guides, system architecture – is solid and handed over properly. A smooth launch is great, but knowing your team fully understands what’s been built is what sets you up for everything that comes after.

Key security and compliance requirements for fintech products

- Regulatory compliance: your partner needs to genuinely understand PCI DSS, GDPR, AML, and KYC, not just recognize the acronyms. Getting this wrong in fintech development outsourcing projects is an expensive mistake.

- Data security: encryption, secure authentication, and strict access controls aren’t negotiable when you’re handling sensitive financial information. If a team isn’t raising this early, that’s a red flag.

- Secure development practices: ask how they actually build, not just what they claim. Good teams follow secure coding standards and catch vulnerabilities before they ship, not after.

- Vendor due diligence: before committing to a fintech outsourced software development company, review their security policies, certifications, and whether they’ve genuinely worked with regulated financial products before.

- Ongoing monitoring: security isn’t a one-time checkbox. Dependable fintech outsourcing services include continuous monitoring, regular audits, and staying current with compliance changes as they happen. A partner who treats security as a launch-and-forget task will eventually become a liability.

Get each of these right, and you’re building on solid ground. Miss even one, and it has a way of catching up with you at the worst possible time.

Common fintech outsourcing challenges & how to overcome them

1. Misalignment in fintech product development goals

This one comes up more than people expect. In fintech development outsourcing, there’s often a gap between what the business thinks is being built and what actually gets delivered. Unclear requirements and shifting scopes are usually the culprits.

Solution: Define your KPIs early, write proper PRDs, and map out user journeys before development kicks off. Build regular feedback loops into your sprints and don’t assume everyone’s on the same page – check in consistently throughout the fintech product development cycle.

2. Weak fintech app architecture planning

Outsourced teams sometimes prioritize shipping fast over building right. For transaction-heavy platforms, that’s a serious risk that shows up later in performance and security problems.

Solution: Get your fintech app architecture guidelines established before full-scale development starts, enforce cloud-native design, and bring senior engineers in to review system design early.

3. Limited access to fintech AI product developers

Finding skilled fintech AI product developers through outsourcing is genuinely hard, particularly for fraud detection, risk modeling, or personalization engines.

Solution: Work with vendors who already have this experience and lean on pre-trained systems and proven frameworks rather than building everything from scratch.

4. Compliance and communication gaps

Regulatory complexity plus time zone friction is a frustrating combination that quietly creates compliance risks and delivery delays.

Solution: Structure your workflows around agile reporting, compliance checkpoints, and shared dashboards. Document regulatory requirements upfront and keep escalation channels clear.

5. Customer experience inconsistencies

Customer support outsourcing for fintech companies can get inconsistent fast – especially without proper domain knowledge or compliance awareness baked into the process.

Solution: Invest in detailed SOPs, fintech-specific training, and AI-assisted support tools. Consistent QA checks and monitoring keep service quality where it needs to be.

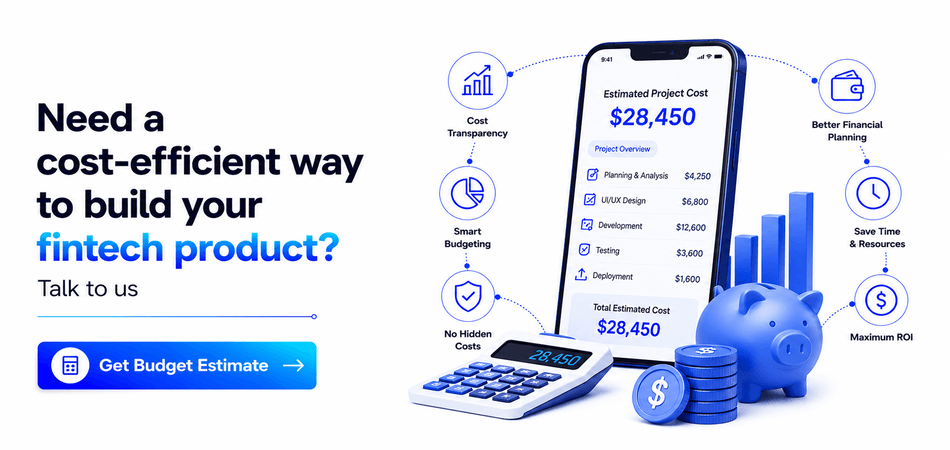

Fintech development outsourcing cost analysis

Understanding the fintech development outsourcing cost is essential for budgeting, especially when building secure and scalable financial products. The cost is not fixed – it depends on project complexity, team location, tech stack, and the scope of outsourcing services you choose.

Typically, outsourcing costs are structured across development stages, with each phase contributing differently to the overall budget.

| Development Stage | What It Includes | Estimated Cost Range (USD) |

| Discovery & Planning | Requirements, compliance mapping, roadmap | $50,000 – $80,000 |

| UI/UX Design | Wireframes, user flows, fintech interface design | $60,000 – $100,000 |

| Architecture Setup | System design, security, scalability planning | $80,000 – $150,000 |

| Core Development | Backend, frontend, APIs, integrations | $120,000 – $250,000 |

| Testing & QA | Security testing, bug fixing, compliance validation | $70,000 – $120,000 |

| Deployment & Maintenance | Cloud setup, updates, monitoring, support | $90,000 – $300,000 |

Summary:

- Small-to-mid fintech products typically start around $50,000

- Complex, enterprise-grade platforms can exceed $300,000+ depending on scale and compliance needs

The biggest cost drivers are usually security requirements, regulatory compliance, and advanced features like fraud detection or AI-based analytics. Choosing flexible fintech outsourcing services can help optimize these costs by allowing you to scale teams up or down based on project needs.

To reduce overall spending, companies often start with an MVP approach, reuse proven fintech modules, and work with experienced offshore teams instead of building everything in-house.

How to choose the right fintech development outsourcing partner

1. Don’t just look at tech, look at fintech thinking

A lot of teams can code, but not everyone understands how money apps actually work in the real world. A good partner should already be tuned into fintech trends like digital banking, embedded finance, and AI-driven financial tools. If they’re not keeping up, your product will feel outdated before it even launches.

2. Ask how they actually build, not just what they’ve built

Instead of just scrolling through portfolios, dig into how they approach architecture. solid team from a mobile app development company in USA style setup will talk about scalability, security layers, and compliance from day one – not as an afterthought.

3. See if they’re ready for the “smart finance” wave

Fintech isn’t just apps anymore – it’s getting more predictive and conversational. If they can work with voice-activated fintech features or build AI-based decision systems, that’s a big green flag. It shows they’re not stuck in old-school development.

4. Compliance talk shouldn’t feel confusing

If a partner starts sounding vague when you ask about security, that’s a red flag. In fintech development outsourcing, things like KYC, encryption, and data rules aren’t optional. The right team explains it clearly instead of overcomplicating it.

5. Communication matters more than people think

Even the best dev team can mess things up if updates are messy. You want someone who’s transparent, shares progress regularly, and actually listens instead of just “reporting progress.”

6. Think long-term, not just launch day

Good partners don’t disappear after delivery. They stick around for updates, scaling, and improvements – basically treating your product like it’s still growing, not finished.

Trends shaping fintech development outsourcing

The fintech outsourcing space is moving fast, and honestly, the businesses keeping up are the ones paying attention to these shifts:

- AI is changing what gets outsourced — it’s not just development work anymore. Teams are outsourcing entire AI-powered workflows like fraud detection, risk scoring, and predictive analytics. Partners who can’t talk about AI fluently are already falling behind

- Compliance is a dealbreaker — regulations are only getting stricter. Businesses are outsourcing to partners who already understand GDPR, PCI-DSS, and open banking frameworks because building that expertise in-house takes time nobody has

- Nearshoring is replacing traditional offshoring — closer time zones mean smoother collaboration, fewer communication gaps, and honestly just better results. The slight cost difference is worth it

- Embedded finance is exploding — retailers, SaaS platforms, and marketplaces all want financial features built fast. That’s creating massive demand for specialized fintech outsourcing partners

- Cloud-native is the baseline now — it’s not a selling point anymore, it’s just expected. Partners still thinking in legacy infrastructure mindsets are getting left behind

Why Techugo is the right fintech development outsourcing partner?

In fintech, even a small architecture mistake can turn into a big business problem later.

That’s precisely where Techugo comes in.

Instead of treating development like a checklist, our team approaches every project with a product-first mindset. Every single project is planned with a clear structure (from backend architecture to user experience) so there are no last-minute fixes when the product starts scaling.

In simple terms, choosing a reliable mobile app development company like Techugo means getting more than just development support – it means having a partner that understands how fintech products need to behave in the real world: fast, secure, scalable, and future-ready.

We also stay aligned with evolving fintech trends, which means modern capabilities like AI-driven automation, smarter financial workflows, and seamless digital experiences can be integrated without rebuilding everything later.

So why wait? Let’s build your fintech product and take it live – just reach out and we’ll take it from there.

FAQs

1. How much does fintech development outsourcing cost?

Costs usually range from $50,000 to $300,000+ depending on complexity, features, compliance requirements, and the expertise of the development team.

2. Why should companies outsource fintech product development?

Companies choose outsourcing to reduce costs, speed up development, and access specialized talent. It also helps them scale faster without building a large in-house engineering team.

3. How long does it take to build a fintech product?

On average, fintech product development can take 3 to 9 months depending on scope, integrations, and regulatory requirements.

4. Is outsourcing safe for fintech applications?

Yes, if you choose a reliable partner. Security, compliance, and data protection standards must be strictly followed to ensure safe and compliant fintech solutions.

Get in touch

We'd love to hear from you.