SA

SA  KW

KW  IE

IE AU

AU UAE

UAE UK

UK USA

USA  CA

CA DE

DE  QA

QA ZA

ZA  BH

BH NL

NL  MU

MU FR

FR

📌 Key Takeaways

- Building a fintech app like Pyypl requires strong security, KYC, AML, and compliance integration for the Middle East market.

- The cost of fintech app development depends on features, integrations, scalability, and AI-powered functionalities.

- Core fintech features include digital wallets, instant payments, multi-currency support, analytics, and fraud detection.

- AI and automation are transforming fintech apps by improving personalization, security, and customer engagement.

- Partnering with an experienced fintech app development company helps businesses launch secure and scalable financial solutions faster.

Not everyone in the Middle East has easy access to banking, and opening an account is not always simple because the process and paperwork are lengthy as well as confusing. It is not even possible for many expats because the requirements are very strict and the systems have been built that way. People there still want to send money, pay bills, and manage daily expenses quickly without any hassle but unfortunately, they are left with very limited options.

And one of the best fintech apps that comes in is Pyypl because Pyypl has removed the need for traditional banking, and therefore the long approvals and the complicated steps are reduced. It is simple; anybody can use it instantly and easily. Users are able to send, spend, and control their money without waiting.

That is why more businesses are trying to build a fintech app in the Middle East like Pyypl. The demand has been growing and investors have a golden opportunity to build a similar app or better.

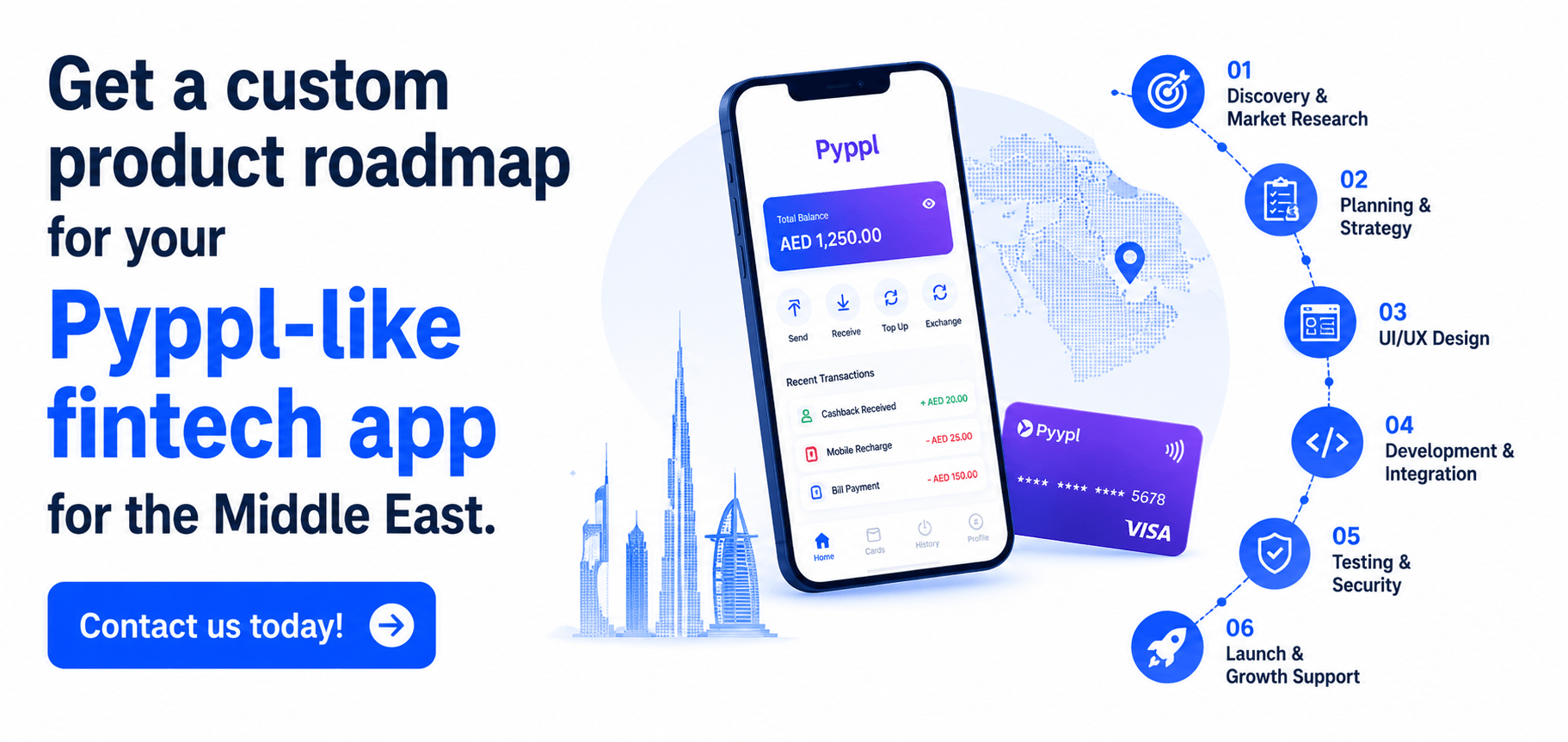

If you want to build a fintech app like Pyypl, then you are not just creating an app but you are solving a real problem and it is something that millions of users have been dealing with for years.

Must Read: AI in Fintech: Driving Innovation in Digital Financial Solutions

What Is Pyypl and Why Is It So Popular in the Middle East?

Pyypl is a fintech app but it is not like the traditional banking apps that people usually see. Pyypl was built for people who do not have easy access to banks and because of that, it removes many of the usual barriers. Users do not need a full bank account, and the process is also very simple so that users can start using it without waiting for days.

It works like a digital wallet where you can store money, send it, and use it for payments. And it also offers a virtual card which means you can shop online but without depending on a physical bank-issued card. This is why digital wallet app development and mobile banking app development are growing fast in the region because users are now expecting faster and easier solutions.

Now, the reason why Pyypl has become popular in the Middle East is not just because of technology, but because it solves a real problem. A large number of expats live and work here and many of them face issues with traditional banking systems, so when an app comes in that is simple, quick, and does not ask for too many details, it naturally gets attention.

And also the region has been moving towards a cashless economy, but at the same time, not everyone was included in the financial system. So Pyypl fits right in between because it connects users to digital payments, therefore it makes everyday transactions easier.

If you are planning to develop a Pyypl-like app, then understanding this user behavior is important because the success is not just about features but about how simple and accessible the experience is.

A Quick Look at Pyypl’s Success

Pyypl started with a simple idea in Abu Dhabi but the app is growing fast. Reason? The problem it solves is real. Over time, the app has grown into a platform that serves users from multiple countries and currencies.

The app has crossed 1 million users. It supports transactions in more than 100 currencies which shows how quickly it has expanded. It has been able to grow its user base and transaction volume consistently due to strong funding rounds and partnerships with global players.

This is exactly why many businesses now want to build a fintech app like Pyypl, because the model has been validated, and the demand is already there. When you develop a Pyypl-like app, you are not starting from scratch, but you are building on a proven idea and adapting it to your audience.

Working with a reliable fintech app development company can help you understand this journey better, because it is not just about features, but about how the product grows… and sustains in the market.

Top 5 Best Fintech Apps Like Pyypl in the Middle East

Pyypl is one of the top fintech apps in the Middle East for payments and money transfers, but it is not the only option. There are several other apps that offer similar services, and exploring them can help you understand what features work best, and what is actually available in your region:

| Best Fintech Apps | Downloads | Ratings |

| STC Pay | 5M+ | 4.7⭐ |

| Mashreq UAE | 1M+ | 4.7⭐ |

| e& money | 1M+ | 4.7⭐ |

| Liv X by Emirates NBD | 500K+ | 4.6⭐ |

| Payit by First Abu Dhabi Bank | 1M+ | 3.6⭐ |

Why Build a Fintech App in the Middle East?

If you look at the data, the Middle East fintech market is growing fast, and it has been expanding steadily over the years. It was valued at around $1.58 billion in 2024, and it is expected to reach $3.9 billion by 2034 (Source: IMARC Group). So the growth is clear but the market is still not fully saturated and therefore there is room for new players.

At the same time, investment is also increasing, and fintech has been one of the top sectors attracting funding. In Q1 2025, $678 million was invested in MENA startups which shows that investors are interested and the ecosystem is becoming stronger.

And it is not just funding, but governments in the UAE and Saudi Arabia are supporting fintech through regulations, sandboxes, and digital initiatives, so that companies can build and scale more easily.

But the real opportunity comes from the users because a large number of expats and underserved populations still face challenges with traditional banking. So when you build a fintech app like Pyypl, you are solving a real problem and not just entering a growing market.

In simple terms, the demand is rising, the support is there and the gap still exists… which makes it the right time to build a fintech app in the Middle East.

Key Features of a Pyypl-Like Fintech App

When you plan to build a fintech app like Pyypl, the features are not just about adding more things, but they are about making the experience simple and fast because users do not want complexity… they want ease and control.

Core Features (Must-Have)

- Easy Onboarding (KYC-lite)

The signup process should be quick, and it should not feel long or confusing because users often leave if it takes too much time, so it needs to be smooth… and clear.

- Digital Wallet

eWallet is the main part of the app, where the money is stored and managed and therefore everything connects to it because without this, the app does not really function.

- Virtual Card

It allows users to pay online, and it is useful especially when they do not have a bank account, so that they can still access digital payments but without restrictions.

Users should be able to send and receive money instantly because that is what they expect now, and if it is slow, then it becomes a problem.

- Bill Payments

This feature makes things easier because users can pay directly through the app, and they do not have to switch platforms, so it improves convenience.

Advanced Features (What Makes You Stand Out)

- AI-Based Fraud Detection

Security is important, and it has been a concern for many users so using AI helps detect unusual activity, and therefore it builds trust… over time.

- Spending Insights and Analytics

When users can see where their money is going, they understand their habits better and it helps them manage finances, but also keeps them engaged.

- Multi-Currency Support

This is useful in the Middle East because many users are expats, and they deal with different currencies so it becomes necessary… not optional.

In the end, when you develop a Pyypl-like app, it is not about adding every feature but about choosing what matters, and building it in a way that is simple because that is what users prefer, and that is what keeps them coming back.

Role of AI in Developing Fintech Apps Like Pyypl

When you build a fintech app like Pyypl, AI is not just an extra feature but it has become a core part of how the app works, because users expect speed, safety, and personalization… and all of that depends on smart systems.

Fraud detection

One of the biggest uses of AI is in fraud detection, because fintech apps deal with sensitive data, and transactions happen in real time. So AI helps monitor patterns and it detects unusual activity instantly, which means the risks are reduced, and users feel more secure.

Behavior analysis

Then there is user behavior analysis where AI tracks how users spend and how they use the app, so that it can offer insights and recommendations. It is useful because users understand their finances better and it also keeps them engaged with the app.

Chatbots and customer support

AI is also used in chatbots and customer support because users want quick answers, and they do not want to wait. So AI-powered chat systems solve queries instantly, and improve the overall experience… without delays.

Credit scoring and risk assessment

And slowly, fintech apps are also using AI for credit scoring and risk assessment, especially for users who do not have a traditional banking history, because it allows platforms to make smarter decisions and expand services.

This is why working with an experienced AI app development company becomes important because building these systems is not simple and it requires the right expertise and understanding of fintech.

In the end, AI is not just supporting fintech apps but it is building the way they function and the way users interact with the app, making them safer and more intuitive.

How to Build a Fintech App Like Pyypl

Creating a FinTech app similar to Pyypl is more than just creating an app-it’s understanding who the end users are, what they require from your application as well as creating a solid backend infrastructure and delivering a seamless user experience.

Step 1: Define Your Target Users

Identifying your target audience is crucial since people from the Middle East have different demographics. The three largest categories of users of mobile wallets are: expatriates, gig economy workers, and people who do not currently have access to traditional banking services. Therefore, while you develop a Pyypl-like app, you should consider simplicity and accessibility.

Step 2: Understand Regulations and Compliance

As we all know that fintech apps must follow strict rules especially in regions like the UAE and Saudi Arabia. KYC and AML processes are important and they cannot be skipped because they directly affect how your app operates… and scales.

Step 3: Choose the Right Tech Stack

Selecting the right technology stack is critical when creating new technologies. With all users expecting fast and secure transactions when using your mobile wallet, you must design a stable and scalable backend, providing all users a responsive and engaging user experience. Digital wallet app development framework will provide you with the foundational components to build a solid backend, which will allow your application to be easily integrated with other 3rd party applications, which expands your application’s user base.

Step 4: Design a Simple and Clear UI/UX

The interface should feel easy because many users may not be familiar with complex financial tools, so the design should guide users and not confuse them… even in small actions.

Step 5: Develop and Integrate Payment Gateway

The Payment gateway is a core feature of the app so payment processing, issuing of cards, and integrating into existing systems must be executed flawlessly as even minor delays can result in a diminishing trust of users.

Step 6: Test for Security and Performance

Fintech apps deal with highly confidential information, therefore testing is imperative. Security auditing and performance tests must occur prior to launch as reliability is very important to users, and are not accepting of any risk.

Step 7: Launch and Improve Continuously

Once your app has successfully launched, you will need to be thinking about future growth and continual improvements through tracking user interaction and further enhancements of functionality, therefore all successful apps begin life as an MVP (minimum viable product) and scale as a consequence of user feedback.

Step 8: Choose the Right Development Partner

Lastly, working with an experienced mobile app development company in Dubai (or your region) will help make your development experience smooth as your developer will have a strong understanding of compliance (laws), integration (connectivity), and scaling (expanding into new markets) from building apps in very complicated markets.

At the end of the day when you build a fintech app in the Middle East, it is not a linear process, but rather one of interconnection because all aspects relating to your app (user, Compliance, Cost, etc.) contribute to the ultimate success of your app as well as the way users perceive your app’s success once it is into the market.

Cost to Build a Fintech App Like Pyypl in the Middle East

When you plan to build a fintech app like Pyypl, the cost is not fixed, and it depends on the features, the complexity, and the level of security, because fintech apps are not simple products… they require strong systems and compliance.

Quick Cost Overview

| App Level | Timeline | Estimated Cost (AED) |

| Basic / MVP App | 2 – 4 months | AED 55,000 – AED 110,000 |

| Mid-Level App | 4 – 8 months | AED 110,000 – AED 260,000 |

| Advanced AI App | 8 – 12+ months | AED 260,000 – AED 550,000+ |

Basic / MVP App

A simple version with core features like wallet, KYC, and transfers can cost around $15,000 – $30,000, and it usually takes less time because the features are limited.

Mid-Level App

With added features like analytics, multi-currency, and better UI/UX, the cost increases to $30,000 – $70,000 because more integrations and testing are involved.

Advanced AI-Based App

If you include AI features, fraud detection, automation, and scalability, then the cost can go beyond $70,000 – $150,000+ and it grows further depending on complexity.

So, the cost to build a fintech app in the Middle East varies, but it is directly linked to what you are building… and how far you want to scale it.

What Affects the Fintech App Development Cost?

- App Complexity and Features – The more features you add, the more the cost increases, because each function needs development, testing, and security layers. A basic app is faster to build, but an advanced app with AI and multiple integrations takes more time and resources.

- Region and Market Requirements – Where you build, and where you launch, both affect the cost. Hiring a mobile app development company in Saudi Arabia can be more expensive than outsourcing to other regions but it also brings better understanding of local compliance and user behavior.

- Development Team and Expertise – The experience of the team matters a lot because fintech apps need strong security and stable architecture. A skilled team may cost more, but it reduces risks and improves the overall quality… which is important in the long run.

- Platform and Technology Choice – Choosing between native and cross-platform development impacts the budget. Native apps offer better performance but they cost more, while cross-platform solutions can reduce cost but may have limitations… depending on the features.

- Integrations and Third-Party Services – Fintech apps depend on multiple integrations like payment gateways, KYC verification, and banking APIs, and each integration adds to the cost because it requires setup, testing, and maintenance.

- Security and Compliance – Security is not optional in fintech, and it requires encryption, data protection, and compliance with regulations. These factors increase the fintech app development cost, but they are necessary because user trust depends on them.

- Post-Launch Maintenance and Scaling – The cost does not stop after launch, because updates, bug fixes, and scaling are ongoing processes. So long-term planning is important, especially when you want to grow your app in the market.

How to Monetize a Pyypl-Like Fintech Application?

When you develop a Pyypl-like app, monetization is not about charging users heavily but it is about small, consistent revenue streams, because users prefer low-cost or free services… but they still generate value over time.

Transaction Fees

You can charge a small fee on transfers, bill payments, or withdrawals, and even a tiny percentage adds up as the user base grows.

Interchange Fees (Card Payments)

When users pay through virtual cards, you earn a share from merchants so this becomes a steady revenue source.

Premium Features

Basic services can stay free, but advanced features like higher limits, faster transfers, or analytics can be paid… so that power users contribute more.

Partner Commissions

You can collaborate with brands and financial services and earn commissions on referrals or in-app purchases.

Currency Conversion Fees

Since many users are expats, charging a margin on currency exchange becomes a strong monetization channel.

In the end, the model works best when it feels light to the user, but consistent for the business because that balance is what makes fintech apps profitable… and sustainable.

Why Choose Techugo for Fintech App Development in the Middle East

Creating a fintech app is not an easy task. You require a team that understands both technology and trust and can help you plan with a complete strategy.

Techugo has real experience in fintech so when you plan to build a fintech app like Pyypl, things feel more structured and less risky. It is a trusted and experienced mobile app development company in UAE and its team well understands local regulations and user behavior which saves time and avoids mistakes.

The team focuses on security because fintech apps deal with sensitive data and that cannot be compromised. Plus, you get end-to-end support so you are not left figuring things out alone during development or after launch.

Creating a fintech application with Techugo means working with a team that understands what you are trying to build… and helps you do it the right way. So schedule your call with fintech app experts today and clear all your doubts.

Frequently Asked Questions

Q. How much does it cost to build a fintech app in the Middle East?

The cost to build a fintech app in the Middle East depends on features, complexity, and security requirements. A basic app can cost around AED 55,000 to AED 110,000, while mid-level apps go higher, and advanced AI-based apps can exceed AED 500,000+. The more integrations and compliance needed, the higher the cost.

Q. How long does it take to develop a fintech app?

It usually takes 2 to 4 months for a basic version, and 6 to 12 months for a full-featured app. The timeline depends on features, testing, and regulatory approvals, because fintech apps require more validation… not just development.

Q. What are the biggest challenges in fintech app development?

The biggest challenges are security, compliance, and user trust. Fintech apps must follow strict regulations, and they handle sensitive data, so even small mistakes can create risks. Integration with payment systems and ensuring smooth user experience can also be complex.

Q. How do fintech apps like Pyypl make money?

Fintech apps earn through small transaction fees, card payments (interchange fees), premium features, and currency conversion charges. The idea is not to charge heavily, but to generate consistent revenue from user activity over time.

Q. Do I need a license to launch a fintech app in the Middle East?

Yes, you usually need a license, because fintech is a regulated space. Countries like the UAE and Saudi Arabia have specific requirements, including KYC and AML compliance. Without proper approval, the app cannot operate legally… so this step is essential.

Get in touch

We'd love to hear from you.